This short-term exchange program lasts for two-four months. A monthly living allowance of NT$16,000 will be provided during the exchange period. A total of one-two spots are available. Both undergraduate and graduate students are eligible to apply, preferably with an engineering background. Applicants should have proficiency in either Chinese (CEFR A2 or above) or English (CEFR B1 or above).

Participants may choose to stay in on-campus dormitories. They may contact the program coordinator in advance to reserve a bed if needed. Alternatively, participants may arrange their own short-term accommodation near the university.

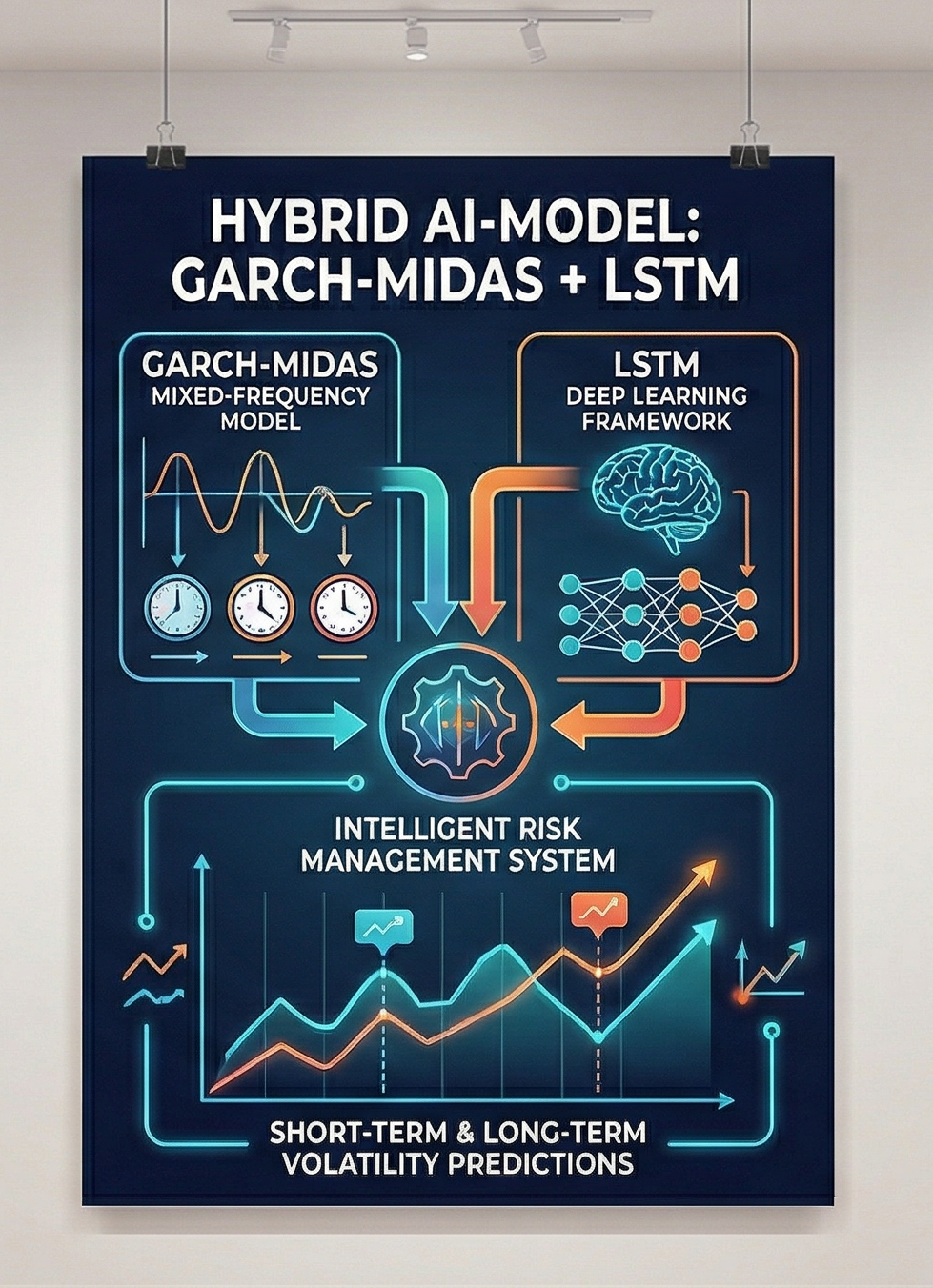

This project aims to recruit outstanding university students from New Southbound Policy countries to Taiwan to study AI application techniques for financial volatility forecasting. By combining the GARCH-MIDAS mixed-frequency model with an LSTM deep learning framework, the project develops an intelligent risk management system with both short-term and long-term volatility prediction capabilities. Students will learn time-series modeling, realized volatility calculation, deep learning algorithms, Python implementation, and financial data analysis, cultivating their FinTech R&D skills and cross-cultural collaboration abilities. A certificate of course completion or internship experience will be provided upon request.

![]()

- Field: Social Science

- School: Da-Yeh University

- Organizer: Department of Finance

- Period of Apply: 2026/04/01-2026/10/31

- Term: 2026/06/01-2026/12/31

- Fee: All participation fees are free of charge. However, participants are responsible for their own round-trip airfare, visa application fees, personal medical and travel insurance, accommodation, daily meals, and any other personal expenses.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

- Contact Person:Yi-Hao Lai

- Email:yhlai@mail.dyu.edu.tw

- Phone:04-8511888 ext 3521